The Consumer IoT's Boon for the Insurance Industry

This story was originally published on the E-Commerce Times on April 30, 2018, and is brought to you today as part of our Best of ECT News series.

Smart home and consumer Internet of Things solutions promise significant opportunities for the insurance industry in terms of reducing costs, alleviating risks, deepening customer engagement, and creating new services and revenue streams. There are many barriers ahead to overcome, but given the tremendous upside, insurance companies have begun attacking these challenges with a multi-tiered strategy.

The currency of these opportunities is data, and the level of integration required to realize the insurtech vision and enhance aspects of the insurance business is a huge undertaking. It requires collecting massive amounts of unstructured data from a variety of connected sources.

The requirements for substantiating requests and implementing regulatory changes to policies and pricing will the involvement of thousands of homes with active devices, control groups, and multiple sources over a period of years for corroboration.

IT Transformation Coming

Many carriers have been running trials and data-gathering efforts through various partnerships for the past few years, but these have been relatively small-scale efforts. Insurance companies will have to transform their IT infrastructure completely to manage the volume, velocity and variety of big data from the IoT solutions installed in their customers' homes and cars. Querying that data at scale will require technology capable of handling hundreds of terabytes.

Finally, integrating that data into the daily workflows of underwriting, claims, customer service, and product development will require the transformation of all related back-end systems.

In light of these challenges, insurance companies have begun developing both short-term and long-term IoT strategies:

- Short-term plans tend to focus on raising consumer awareness, generating measurable results for marketing and sales, and deepening customer engagement to pave the way for future products and services.

- Long-term strategies provide a road map for implementing the technology and forming the partnerships required to bring a complete insurance IoT solution to market at scale, and to operationalize the data in every aspect of a firm's core business.

Insurers have taken a variety of progressive actions to leverage IoT for marketing and sales. For example, State Farm has a dedicated Web page that includes educational content and special offers for specific security products and monitoring solutions. Travelers has offered several special offers from August Home, Canary, Roost, Vivint, Piper and Nest Protect.

Consumer Education

One key aspect of short-term plans is consumer education. While insurance consumers generally are aware of their own costs and coverage, they are less familiar with the factors that influence insurance costs. Similarly, they recognize the benefits of smart home products, but in general are not yet persuaded that the value exceeds their cost.

Consumer awareness actions on the part of top insurance companies include the following:

- Consumer education programs on digital media promoting the value propositions of smart home devices.

- Recommendations of specific smart home solutions, often with special pricing offers, as part of larger co-marketing campaigns in conjunction with retailers, OEMs and service providers.

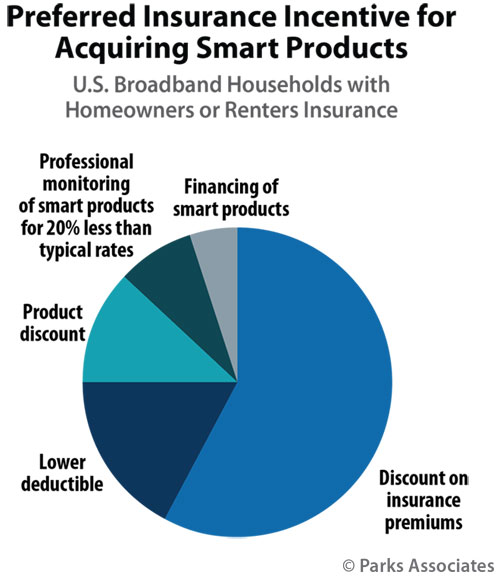

- Soft and hard home insurance premium discounts for installing smart devices. Soft discounts for installing smart devices are offered as incentives policyholders can "discuss with their agent." They become part of the negotiating process for renewals or new policy holders. Hard discounts are offered as a fixed percentage off all or a portion of the home insurance premium, much like "security" discounts have been offered for installation of a monitored security system. Validation of a working device may or may not be required.

- Free devices, such as smart smoke detectors or water leak sensors, are offered to attract new policyholders. Some free device programs are offered to existing policyholders as both retention efforts and data gathering and risk mitigation trials.

- Lead-generation efforts and data mining to identify and target owners of smart home solutions as potential policyholders with lower risk assessments.

Insurers and smart home manufacturers have an opportunity to create mutually beneficial partnerships that can increase adoption of smart home solutions and build engagement with consumers.

Partnerships in the insurance areas leverage data from smart devices to enhance customer benefits and awareness, including providing more transparency around premiums, personalizing policies, and reducing risk for customers.

For smart home players, partnering with the insurance industry can help extend the value propositions of their solutions, in addition to driving adoption.

Among U.S. broadband households, there already is considerable consumer interest in smart home solutions.

Currently, 26 percent of U.S. broadband households have at least one smart home device, and more than 50 percent plan to buy a smart home device in the next 12 months.

System Integration

With a variety of devices going online, a key challenge in the smart home industry will be to integrate these devices into a system in which device categories interoperate and share data to create a personalized and valuable experience for the end users.

These types of negotiations among smart home players can get bogged down in territorial battles, with companies often unwilling to cede ground to perceived competitors. That can create problems, as consumers expect ease of use and interoperability in their devices.

In this respect, the data needs of insurance companies are not aligned with the current fragmentation in the market. They need a clear, standardized process for aggregating data from a variety of devices and services.

Large players may negotiate and manage a variety of relationships with data collectors, but medium to smaller players will require an intermediary to manage the task. Of great benefit would be a standardized schema and app tool for sharing insurance-related data points with one's insurer. Consumers are ready for such advances:

- Almost 60 percent of consumers are likely to purchase a smart home product that can either detect, notify of, or prevent damage or loss due to water, fire, or theft.

- Roughly 75 percent of respondents willing to purchase a smart product are willing to let the devices automatically communicate with insurance companies.

- Nearly 40 percent of consumers report they would switch insurance providers in order to obtain smart home products.

Security and safety are key drivers in smart home adoption, and they can serve as a broader force in integrating all areas of the smart home. In the end, all parties, including the consumer, benefit when the rich data sets generated by smart home solutions are accessible across categories.

As technology continues to advance, more progressive actions will occur around the operationalization of IoT, including more VC investments, employee trials with connected devices to help define data collection aspects, and pilots with small groups of homes. The process will not be easy, but both short- and long-term benefits will make these efforts worthwhile and ultimately rewarding. ![]()

The opinions expressed in this article are those of the author and do not necessarily reflect the views of ECT News Network.

from TechNewsWorld https://ift.tt/2BEAHxC https://ift.tt/2KHtGPs

via IFTTT

ذات الصلة

اشترك في نشرتنا الإخبارية

Post a Comment